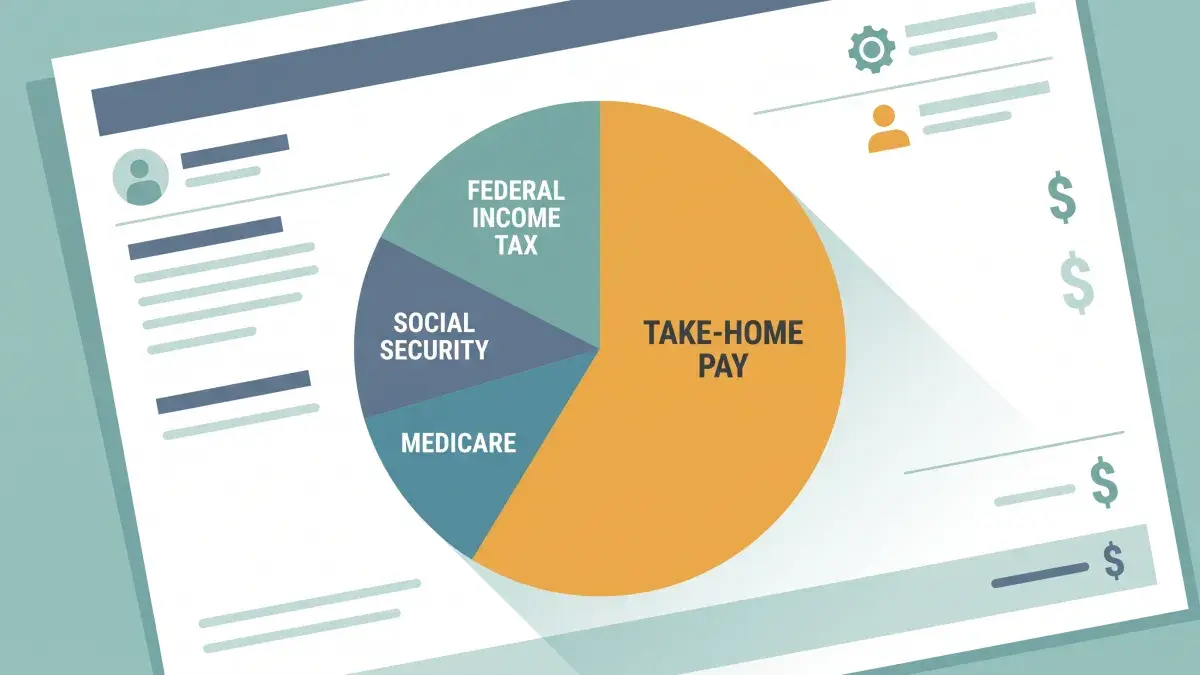

How Much Taxes Are Taken Out of My Paycheck?

A typical US worker keeps roughly 70–85% of gross pay after taxes. Every paycheck loses federal income tax (a progressive 10–37% marginal rate on taxable income), Social Security (6.2% up to the annual wage base, $184,500 in 2026), and Medicare (1.45% on all wages), plus state income tax in the 41 states that levy one. On a $75,000 single-filer salary in a no-income-tax state, about $12,800 — 17.1% of gross — goes to federal tax and FICA, leaving roughly $62,200 in take-home pay.

That is the short answer. But “how much is taken out” depends on your salary, filing status, state, and W-4 choices. Below is exactly what comes out, the 2026 rates from the IRS and Social Security Administration, and a take-home table so you can find your number.

The Four Things Taken Out of Every Paycheck

| Deduction | 2026 Rate | Applies To | Cap |

|---|---|---|---|

| Federal income tax | 10% – 37% (progressive) | Taxable income (gross minus deductions) | None |

| Social Security (OASDI) | 6.20% | Gross wages | $184,500 wage base |

| Medicare | 1.45% (+0.9% over $200K) | Gross wages | None |

| State income tax | 0% – 13.3% | Taxable income (varies by state) | Varies |

Social Security and Medicare together are called FICA (the Federal Insurance Contributions Act) and add up to a flat 7.65% of wages under the cap. For a deeper split of these two, see FICA vs federal income tax. Your employer matches the full 7.65% out of its own pocket, so the government collects 15.3% total on your wages — you only see half on your stub.

Part 1: FICA — The Flat 7.65%

FICA is the easy part because it is flat. Every non-exempt worker pays:

- Social Security: 6.2% of gross wages, up to the 2026 wage base of $184,500. That caps your Social Security tax at $11,439 for the year. Earn more and the 6.2% line simply stops once you cross the base. The Social Security Administration sets the base each October — it was $176,100 in 2025 and rises with the national average wage index (SSA Contribution and Benefit Base).

- Medicare: 1.45% of every dollar of wages, no cap. Workers earning over $200,000 (single) or $250,000 (joint) pay an Additional Medicare Tax of 0.9% on the excess, which the employer does not match (IRS Additional Medicare Tax Q&A).

Part 2: Federal Income Tax — The Progressive Part

Federal income tax is where the “how much” really varies. It is progressive: only the income inside each bracket is taxed at that bracket’s rate. The 2026 single-filer brackets, per IRS Revenue Procedure 2025-11:

| Rate | Single Filer | Married Filing Jointly |

|---|---|---|

| 10% | $0 – $12,400 | $0 – $24,800 |

| 12% | $12,401 – $50,400 | $24,801 – $100,800 |

| 22% | $50,401 – $107,450 | $100,801 – $214,900 |

| 24% | $107,451 – $205,150 | $214,901 – $410,350 |

| 32% | $205,151 – $260,450 | $410,351 – $520,950 |

| 35% | $260,451 – $651,150 | $520,951 – $781,450 |

| 37% | $651,151+ | $781,451+ |

Before the brackets apply, the standard deduction comes off your gross: $16,100 for single filers, $32,200 for married filing jointly in 2026. So a single worker earning $75,000 is taxed on $58,900, not $75,000. Your marginal rate is the bracket your last dollar lands in; your effective rate is total tax divided by gross, always lower.

Part 3: How Much Comes Out at Each Salary

Here is the combined federal income tax + FICA bite for a single filer taking the standard deduction in 2026, and the resulting take-home in a state with no income tax (Texas, Florida, Nevada, and six others). Add your state’s income tax on top where applicable.

| Gross Salary | Federal Income Tax | FICA (7.65%) | Total Federal + FICA | Take-Home (No-Tax State) | You Keep |

|---|---|---|---|---|---|

| $40,000 | $1,900 | $3,060 | $4,960 | $35,040 | 87.6% |

| $60,000 | $4,780 | $4,590 | $9,370 | $50,630 | 84.4% |

| $75,000 | $7,075 | $5,738 | $12,813 | $62,187 | 82.9% |

| $100,000 | $13,170 | $7,650 | $20,820 | $79,180 | 79.2% |

| $150,000 | $25,070 | $11,475 | $36,545 | $113,455 | 75.6% |

| $250,000 | $54,050 | $13,389* | $67,439 | $182,561 | 73.0% |

*At $250K, Social Security caps at $184,500 × 6.2% = $11,439; Medicare adds 1.45% on all wages plus the 0.9% surtax on the amount over $200K. Figures use standard deduction, single filer, no pre-tax deductions. Model your exact salary, state, and filing status in the take-home pay calculator.

Part 4: State Income Tax — The Wild Card

FICA and federal tax are identical in all 50 states. State income tax is not. Nine states levy none: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. The rest run from low flat rates to California’s 13.3% top marginal bracket. On a $100,000 salary, a no-tax state leaves you the full $79,180 above; California would take roughly $5,000–$6,000 more. Compare all of them in our state-by-state take-home ranking.

Part 5: Why Your Actual Check May Differ

The table shows tax. Your real deposit is usually smaller because of voluntary deductions that also leave the check: 401(k) contributions, health and dental premiums, HSA/FSA contributions, and disability insurance. The upside is that pre-tax versions of these reduce the tax in the table — a traditional 401(k) dollar dodges income tax, and an HSA dollar through payroll dodges FICA too. That is the single biggest lever most workers have over “how much is taken out.”

The number of checks matters for how the bite feels, not the annual total: the same tax is spread across 52 weekly, 26 biweekly, 24 semi-monthly, or 12 monthly checks. See how many paychecks are in a year for the per-check math. And if you pick up extra hours, note that overtime is calculated at 1.5× your regular rate but taxed at the same rates as everything else.

Part 6: Taxes in Retirement Are Different

The withholding on your paycheck today funds Social Security and Medicare you draw on later. How much you need to save so those benefits plus your own savings actually cover retirement is its own calculation — our sister site walks through it in how much do I need to retire.

Sources and Methodology

FICA rates and 2026 Social Security wage base: SSA Contribution and Benefit Base. Federal tax brackets and standard deduction: IRS Revenue Procedure 2025-11. Withholding mechanics: IRS Publication 15-T. Additional Medicare Tax: IRS Q&A. All calculations are single filer, standard deduction, no pre-tax deductions unless noted. Last updated July 8, 2026.

Frequently Asked Questions

See Exactly What Comes Out of Your Paycheck

Enter your salary, state, and filing status. The calculator splits out federal income tax, Social Security, Medicare, and state tax, then shows your take-home per paycheck. Free and instant.

Open Take-Home Calculator →